NEWSLETTER

In January, we enrolled in the ChaiTech accelerator, to showcase InvestLens to investors. We are also bringing on individuals with decades of expertise in R&D, marketing, and data analytics. In addition, the platform now supports enterprise clients through a backend administrative console and client-facing billing and user management. We integrated Stripe to help ensure client payment data remains secure. Access to the platform remains free of charge, but the tools are available for testing.

- All accounts are transformed into organizations. They support four roles: Member, Billing, Admin, and Owner.

- For members with Billing or Owner roles, the profile menu in the main UI now includes a Billing tab. This allows users to select the appropriate plan (for example, Individual vs. Group).

- For members with Admin or Owner roles on a Group plan, an Organization Console tab is available in the main UI. This enables organizations to manage members and set permissions.

- The platform is integrated with Stripe, currently operating in sandbox mode (real credit cards are not accepted).

Platform updates

We found that mainstream methods for estimating implied volatility, a forward-looking indicator of risk, come with limitations, including sensitivity to sparse or noisy option data and simplifying assumptions that can break down in real markets. Addressing these issues requires careful modeling choices and extensive validation, so this work is taking longer than we initially expected.

We continue working on our approach to estimating implied volatility with the goal of resolving some of these limitations. We plan to use these enhanced estimates in reporting, since many portfolio managers view implied volatility as more trustworthy than purely historical measures.

Analytics in Practice

Last month we built a focused US Financials basket for broad sector coverage that is not riskier than the overall equity market. Using the Universe Screener (Custom tab), we defined “slices” of the market by combining country, benchmark, and sector filters, as shown in the table below (US Financial Services was drawn primarily from IXF, with a small complement from S&P 100 Financials).

We employed the Universe Screener and converted our idea into a new portfolio. Position weights were constrained to 2%–12% (0.02–0.12), preventing holdings from becoming immaterial or overly concentrated contributors to risk. The portfolio was titled US IXF SP100.

We then ran the portfolio through the Asset Allocator to optimize weights under our selected constraints. We saved the max Sharpe Ratio portfolio as US IXF SP100: Max Sharpe Ratio Portfolio.

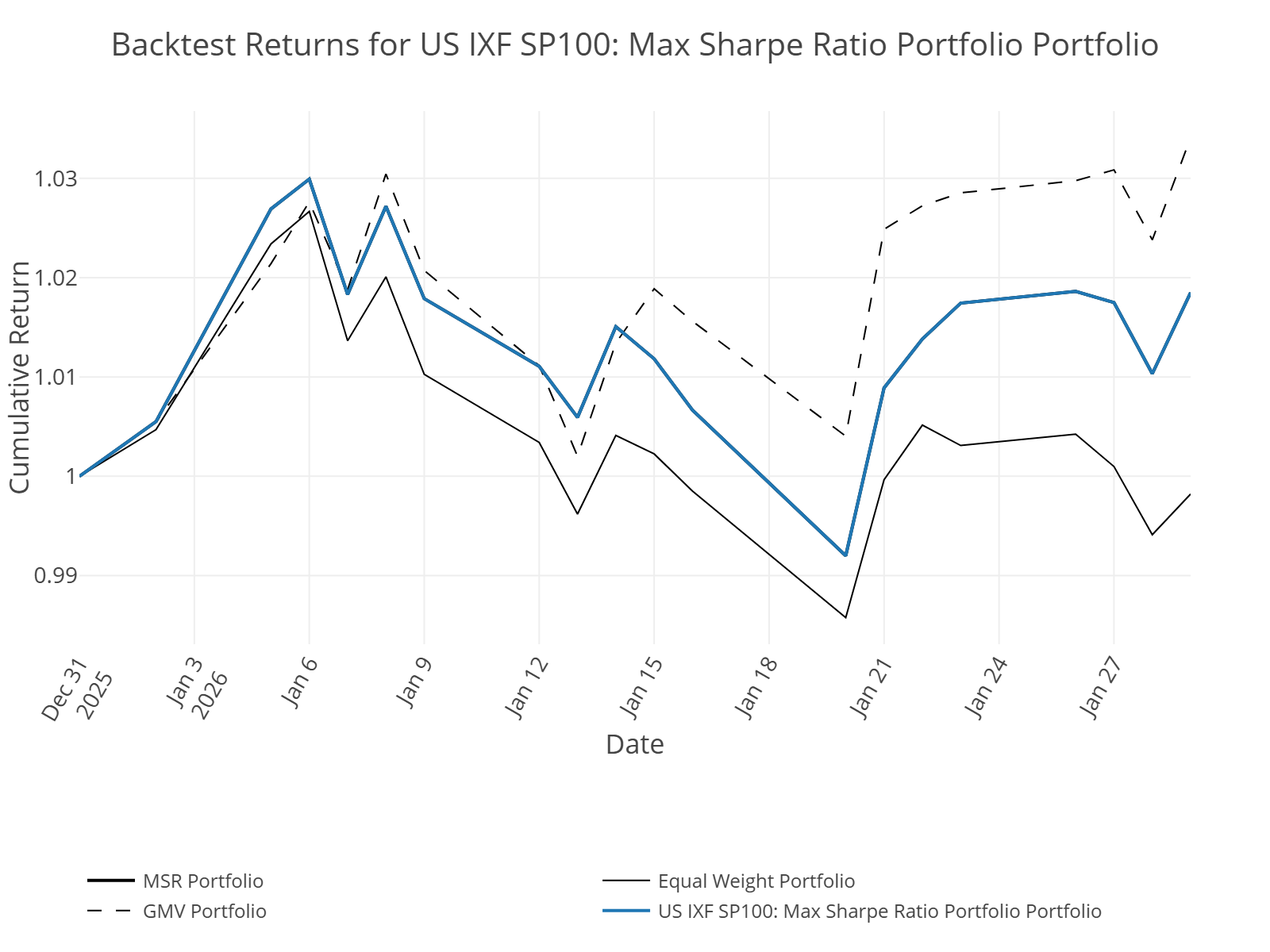

Since initial construction, InvestLens was tracking US IXF SP100: Max Sharpe Ratio Portfolio. The plot above shows cumulative returns from the end of December 2025 through late January 2026 for four weighting schemes: the baseline basket (blue), which is nearly indistinguishable from the MSR portfolio over most of the window, plus equal-weight and GMV.

After an early rise into the first week of January, the portfolios experience a mid-month pullback and then diverge sharply. GMV finishes the period on top, with the strongest late-January rebound, while the baseline/MSR line ends positive but below GMV. The equal-weight portfolio trails, showing deeper drawdowns and a weaker recovery by the end of the window.

In conclusion, the Global Minimum Variance portfolio can outperform “chasing” maximum expected returns, especially when volatility is elevated. Using the optimizer and a backtest over the last month, we see that the Maximum Sharpe Ratio (MSR) portfolio still outperforms a naïve equal-weight approach, even in a choppier regime where diversification alone is not enough. That matters because January was packed with event-driven headlines, from geopolitical flare-ups and trade rhetoric to widely covered disputes like the Greenland-related tensions. This is a useful reminder that risk control can be a return driver, and disciplined optimization can beat simple heuristics without relying on calm markets.